Should new Jacksonville residents rent or buy after relocating?

Rent first if you’re still learning the area or expect to move again within about three years, and buy once you know where you want to be and plan to stay five years or more. With Jacksonville’s median sale price near $314,900 and 30-year rates at 6.55%, that time horizon usually decides renting vs. buying in Jacksonville more than the monthly payment does.

Why relocating to Jacksonville makes this decision harder

When you move to a new metro, you’re making two big calls at once: where in the region to live, and whether to rent or own. Get them out of order and it gets expensive. Buying in a part of town that turns out to be a rough commute, or one that doesn’t fit your day-to-day, can cost far more than a year of rent once you factor in the cost of selling again.

Jacksonville spans a lot of ground. The city sits in Duval County, but the wider market pulls in St. Johns County to the south (Ponte Vedra, Nocatee, St. Augustine), Clay County to the west (Orange Park, Fleming Island), and Nassau County to the north (Yulee, Fernandina Beach).

Rents, prices, taxes, and commute times vary across those lines. In closings I’ve handled for out-of-state buyers, the ones who rented for a few months first almost always bought with more confidence.

The good news: the local math is knowable, and the numbers below make the trade-offs clear.

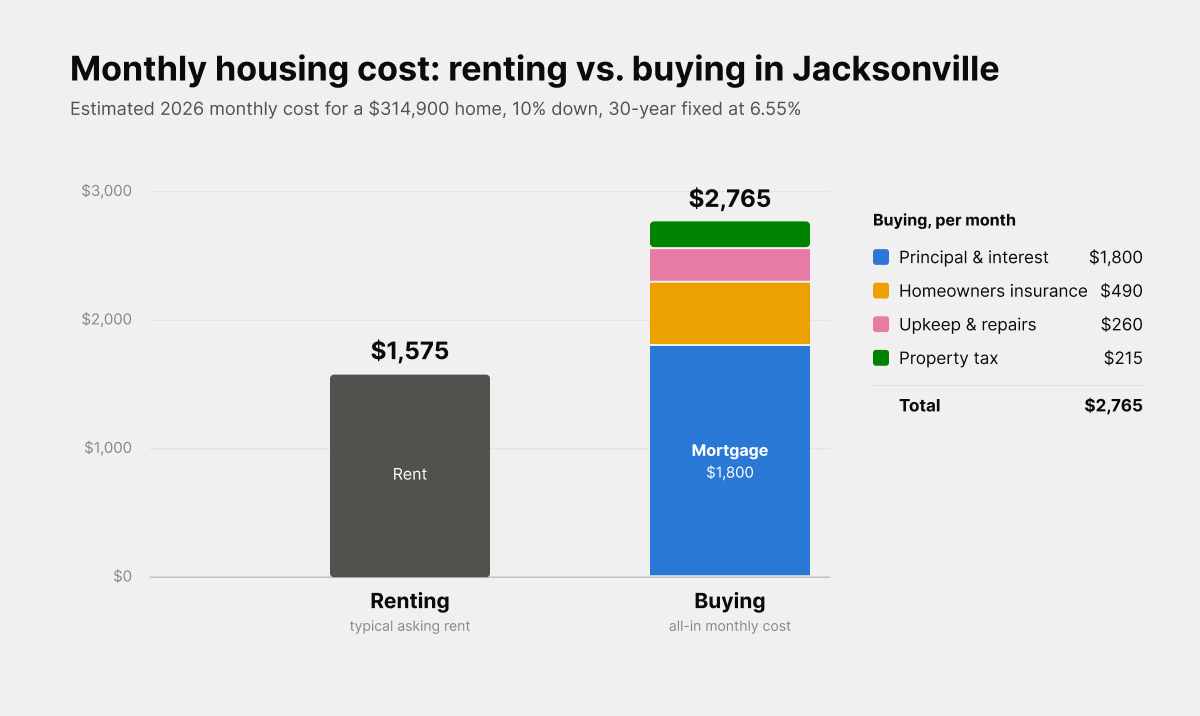

What does it cost to rent vs. buy in Jacksonville right now?

Renting costs less month to month today; buying costs more up front and monthly but builds equity and locks your payment.

As of mid-2026, the average asking rent in Jacksonville is roughly $1,575 a month, according to Zumper (July 2026); other trackers put the median rent closer to $1,300, such as Apartment List (early 2026), with the gap coming down to method and unit mix.

The median home sale price was about $314,900, per Redfin’s Jacksonville market report (June 2026), and the average 30-year fixed mortgage rate sat at 6.55%, according to Freddie Mac (July 16, 2026). On a home at that price with 10% down, your principal and interest land near $1,800 a month before taxes, insurance, and upkeep.

The two paths compare like this for a typical Duval County move:

| Factor | Renting a typical home | Buying a $314,900 home (10% down) |

|---|---|---|

| Upfront cash | First month + deposit, roughly $3,000–$5,000 | Down payment + closing costs, roughly $40,000–$50,000 |

| Rough monthly housing cost | ~$1,575 (Zumper, July 2026) | ~$2,500–$2,800 all-in (P&I at 6.55% + taxes + insurance + upkeep) |

| Payment stability | Resets at each lease renewal | Principal and interest fixed for 30 years |

| Builds equity | No | Yes, over time |

| Who handles repairs | The landlord | You |

| Flexibility to move | High | Lower; selling runs about 7–9% of price |

Two Jacksonville-specific line items widen that monthly gap, so build them into your budget from the start:

1. Homeowners insurance. Florida premiums run high. Bankrate put the state average near $5,838 a year for $300,000 in dwelling coverage in 2026, more than double the national figure. Flood zone, roof age, and build year move your quote a lot, so get a real number before you write an offer.

2. Property taxes and CDD fees. Your tax bill depends on the county, the millage rate, and your homestead exemption. Newer planned communities, common in St. Johns County, can also carry a Community Development District fee that isn’t in the list price. I break that down in what CDD fees mean for Jacksonville buyers.

Sources: rent, Zumper (Jul 2026); price $314,900, Redfin (Jun 2026); rate 6.55%, Freddie Mac (Jul 2026); insurance, Bankrate (2026). Property tax and upkeep are estimates; your figures vary by county, homestead exemption, flood zone, and roof age. Figures rounded.

When does renting make more sense after a move?

Renting is usually the stronger first move when your plans, your budget, or the neighborhood are still up in the air. It buys you time and keeps you flexible while you learn the market firsthand.

Rent first if several of these fit you:

1. You’re not sure where you’ll settle. A short lease lets you test commutes to your actual job, try a couple of areas, and avoid buying in the wrong spot.

2. You might move again within three years. Selling costs (agent fees, closing costs, prep) often eat any short-term appreciation, so a quick turnaround favors renting.

3. Your down payment and reserves aren’t there yet. Buying while cash-thin leaves nothing for the insurance deductible or the first repair.

4. Your income is new or variable. Lenders want stability, and so does your own peace of mind, in the first year at a new job.

5. You want to shop rates. With rates in the mid-6s, some buyers rent a year and watch for a better financing window rather than locking in under pressure.

Renting isn’t “throwing money away.” You’re paying for flexibility and for time to make a six-figure decision well.

When does buying make more sense in Duval County?

Buying tends to win once you’re staying put and your finances are steady, because a fixed mortgage stops your housing payment from climbing at every lease renewal while you build equity.

Jacksonville’s current conditions help patient buyers: inventory sat near 4.3 months of supply with about 10,400 active listings in May 2026, and homes took a median of roughly 60 days to sell, based on regional market data (Redfin, 2026).

More choices and slower sales mean less bidding-war pressure than a few years back.

Buying is often the better fit when:

✓ You’ll stay five years or more. That’s typically enough time for appreciation and paydown to clear your buying and selling costs, though it’s a guideline, not a guarantee.

✓ You have stable income and a real down payment, plus a cushion for Florida insurance and maintenance.

✓ You want to lock your housing cost. A fixed payment is a hedge against future rent increases.

✓ You’ve picked your area. You know your commute, your county, and the trade-offs between, say, an established Duval County neighborhood and a newer St. Johns County community.

A note I give every relocating client: don’t let “rates are high” alone talk you out of a home you’ll keep for a decade. You can often refinance a rate later; you can’t go back and buy at today’s price if values rise.

That’s professional insight, not a promise, so run your own numbers with a lender.

How should you decide?

Work through five questions in order, and the answer usually settles itself:

1. How long will you stay? Under 3 years leans rent; 5+ years leans buy. The in-between is a judgment call.

2. Do you know where you want to live? If not, rent in the general area and narrow it down on the ground.

3. Is your cash ready? Add up down payment, closing costs, and a reserve for insurance and repairs. If it’s tight, keep renting and keep saving.

4. Is your income stable? A steady paycheck strengthens your loan terms and your budget.

5. Does the all-in monthly cost fit? Compare real rent quotes against a real ownership estimate, taxes and Florida insurance included, not principal and interest alone.

If you’re relocating from out of state, this is also the moment to line up the sale of your current home with the timing of your next one. I do that across state lines for clients moving between markets, which you can read about on the relocation planning page.

For the wider local picture, the Jacksonville real estate guide and my 2026 Jacksonville housing market breakdown go deeper on prices, inventory, and neighborhoods across Duval, St. Johns, Clay, and Nassau counties.

Renting vs. buying in Jacksonville FAQs

Is it cheaper to rent or buy in Jacksonville in 2026?

Month to month, renting is cheaper today: the typical asking rent is about $1,575, while all-in ownership on a median-priced home runs closer to $2,500–$2,800. Buying tends to pay off over a longer stay through equity and a fixed payment.

How long should I rent before buying after relocating?

Often three to twelve months. That’s usually enough to confirm your commute, choose a county and neighborhood, and get your down payment and reserves in place.

How much do I need to buy a $315,000 home here?

Plan for roughly $40,000–$50,000 with 10% down plus closing costs, and keep a separate cushion for Florida homeowners insurance and early repairs.

Do Jacksonville property taxes and insurance change the rent-vs-buy math?

Yes, by a lot. High Florida insurance and county-specific taxes can add several hundred dollars a month to ownership, so compare the all-in cost, not the mortgage payment alone.

What’s the right next step for your move?

The honest answer to renting vs. buying in Jacksonville depends on your timeline, your cash, and the exact area you land in, so the smartest first move is to price out both paths with real local numbers before you commit.

Bring your target neighborhoods, your budget, and your move date, and we’ll build a side-by-side comparison for your situation across Duval County and its neighbors.

Ready to run your numbers? Email Nia at listwithnia@gmail.com and you’ll get a rent-versus-buy breakdown built on current Duval County figures. As a Realtor licensed in Florida, Illinois, and Georgia with LPT Realty, Nia helps new residents settle into Jacksonville on a timeline that fits their plans, not a sales pitch.